Share This Article

Article Summary

In 2026, Cincinnati is experiencing a rapid increase in bank branch closures as financial institutions consolidate operations and prioritize cost-effective digital platforms. Ohio currently ranks second nationwide for closures, creating banking deserts that disproportionately impact older adults, rural communities, and cash-reliant small businesses. To adapt, banks are transitioning their remaining physical locations from basic transaction centers into specialized financial advisory hubs.

The recent surge in Cincinnati bank closures is dramatically reshaping the local financial landscape.

Many residents are navigating these Cincinnati bank closures by rapidly adopting new digital financial tools.

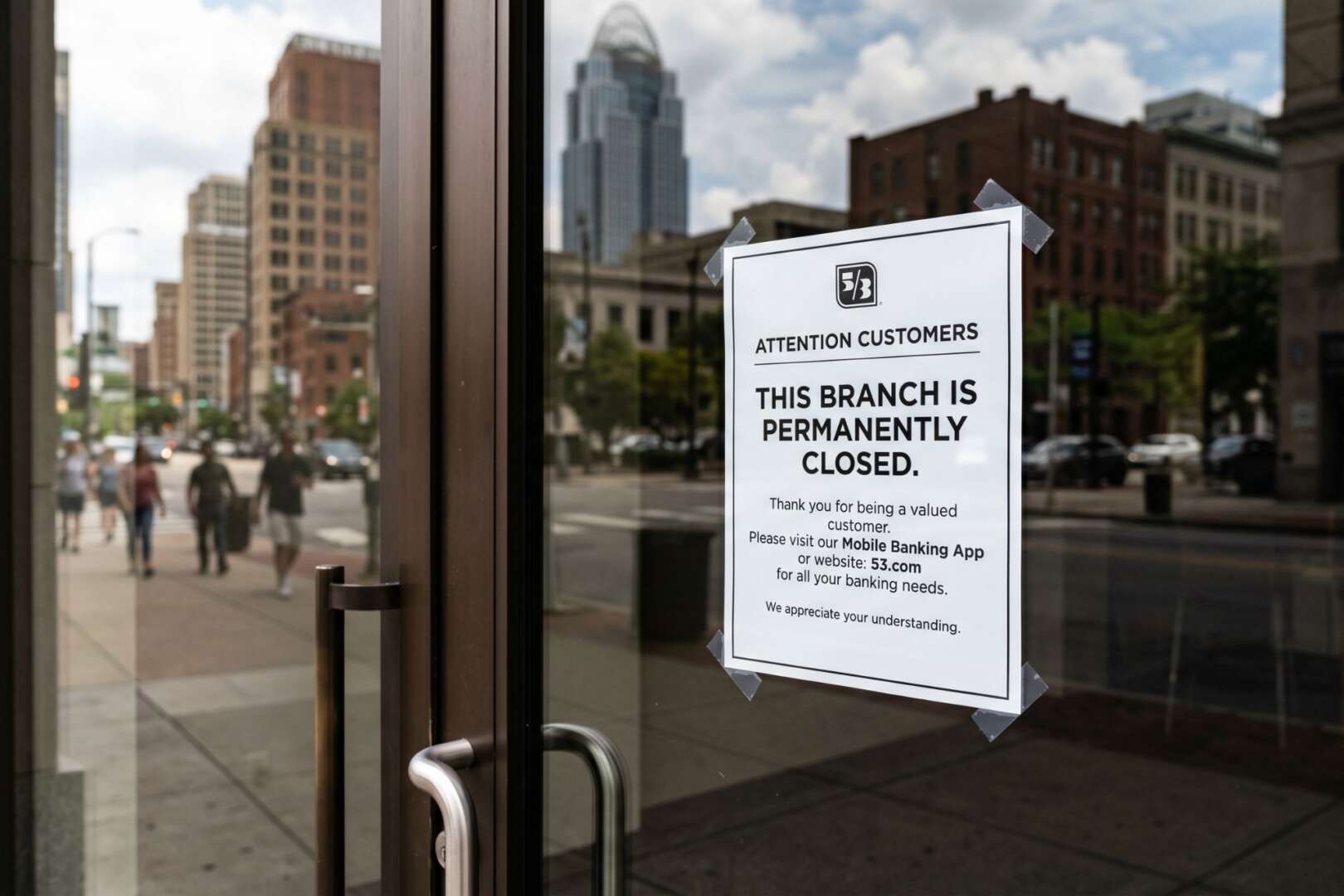

The number of Cincinnati bank closures is rising rapidly in 2026. Major financial institutions are shutting down physical branches across the city. This trend reflects a broader national shift toward online financial services. Ohio ranks second nationwide for branch closures this year. At least 41 branches closed across the state in the first three months alone. TheStreet recently reported these numbers using data from the Office of the Comptroller of the Currency.

Local bank customers must now rely more heavily on mobile apps. Traditional face-to-face banking operates more like a premium service today. Many residents feel the sudden impact when their neighborhood branch locks its doors. This transition forces older adults and small business owners to adapt quickly. We recently covered similar transitions in our report on recent shifts in local commerce. The convenience of online tools cannot fully replace a trusted local banker.

Why Cincinnati bank closures are increasing this year

Industry consolidation acts as the primary driver behind these local shutdowns. Bank mergers picked up significant momentum in late 2025 and continue strongly into 2026. Merging banks often eliminate overlapping branches to reduce overhead costs. Physical locations represent the largest operational expense for modern financial institutions. Running a traditional branch simply costs too much compared to digital alternatives. Banks save millions of dollars annually by trimming their physical footprints.

The cost difference between physical and digital transactions remains staggering. Processing a transaction inside a branch costs a bank around $4.00 on average. Conversely, a digital transaction costs the bank merely four cents. This massive financial incentive makes physical locations less appealing to corporate executives. Financial leaders prioritize efficiency and profit margins over maintaining a massive physical presence. Consequently, banks aggressively push their customers toward mobile platforms.

Several major banking chains have reduced their presence in Ohio recently. PNC Bank announced branch closures across Ohio, Wisconsin, and Missouri late last year. The Economic Times reported these closures as part of a national corporate strategy. JPMorgan Chase and U.S. Bank also consolidated their branch networks recently. These latest Cincinnati bank closures reflect a broader national banking strategy. Cost-cutting measures allow these institutions to invest heavily in robust cybersecurity. Protecting customer data online now requires billions of dollars in annual funding.

Digital banking replaces the traditional branch experience

Consumers drive this transition through their changing daily habits. Mobile check deposits now account for nearly three-quarters of all deposit transactions. Most young professionals rarely visit a physical bank location for everyday needs. The average foot traffic at traditional bank branches dropped significantly over the past five years. People prefer the convenience of managing their money directly from their smartphones. This digital dependency reached an all-time high of 71 percent this year.

Customer service interactions also moved swiftly into the digital realm. Live chat and artificial intelligence inquiries now heavily outnumber in-branch visits. Virtual assistants resolve basic account issues within seconds. Customers appreciate skipping the long lines at the local teller window. However, resolving complex financial problems still requires essential human intervention. Many banks now offer hybrid models blending virtual support with appointment-only branch visits.

Financial institutions heavily promote their enhanced automated teller networks. Modern ATMs handle complex transactions that previously required a human teller. Customers can cash checks, deposit large amounts of cash, and transfer funds instantly. Banks frequently place these advanced machines in high-traffic retail areas. U.S. Bank recently noted they are providing ATMs in local grocery stores following branch closures. This strategy attempts to maintain a physical touchpoint without full branch overhead.

How Cincinnati bank closures affect rural and urban neighborhoods

The impact of Cincinnati bank closures affects communities quite differently. Rural areas and lower-income urban districts face a disproportionate burden during these shutdowns. The Federal Reserve highlighted growing banking deserts across the Midwest in recent reports. A banking desert occurs when a community lacks access to a nearby physical bank. These closures make operating smoothly very difficult for cash-heavy small businesses.

Older adults face unique challenges when their local branch shuts down. Seniors increased their digital banking usage recently, yet they remain the most branch-reliant demographic. Many older residents prefer dealing with a familiar face regarding their life savings. Transitioning to a mobile app feels overwhelming and insecure for this population. Community advocates express deep concerns about financial exclusion for vulnerable residents. Local officials urge banks to reconsider completely abandoning these underserved neighborhoods.

Some banks are testing creative alternatives to mitigate these pressing issues. A few institutions deploy mobile branch vans to visit remote areas weekly. Other banks partner with local post offices or community centers for basic services. While helpful, these temporary solutions do not fully replace a permanent banking location. Customers often drive much further just to access essential financial services. Community leaders hope to slow down these Cincinnati bank closures through local advocacy.

Finding alternative ways to manage your money locally

Cincinnati residents still maintain viable options for managing their finances locally. Community banks and credit unions continue to maintain a strong physical presence. These smaller institutions prioritize customer service and community engagement over aggressive expansion. Credit unions operate as non-profit cooperatives, allowing them to offer better interest rates. Switching to a local credit union provides the face-to-face interaction many customers miss. You can explore how local enterprises adapt in our guide to small business financial strategies.

You should evaluate your daily banking habits before switching financial institutions. Determine how often you genuinely need to speak with a human teller. Consider the types of transactions you perform on a regular weekly basis.

- Do you deposit large amounts of physical cash frequently?

- Do you regularly require official cashier’s checks or certified money orders?

- Do you rely on a safe deposit box for storing important documents?

- Finding a local branch remains essential if you answered yes to these questions.

Customers choosing digital-only banks must carefully review the provided services. Online banks often offer high-yield savings accounts due to their lower overhead costs. However, depositing physical cash into a digital-only account frequently causes major frustration. Many online banks require you to use third-party retail locations for cash deposits. These partner retail locations frequently charge a hefty fee for this deposit service. Always read the fine print before committing entirely to a digital banking experience.

What the future holds for physical bank branches

The physical bank branch continues evolving rather than completely disappearing. Future branches will look vastly different from the traditional banks of the past. Banks redesign their spaces to function more like exclusive financial advisory centers. Financial consultants offering specialized advice will replace tellers processing routine transactions. Customers will visit branches primarily for mortgages, retirement planning, and wealth management discussions. The focus shifts entirely from basic transactions to complex financial problem-solving.

This transformation requires bank employees to develop completely new skill sets. Banks actively retrain traditional tellers as comprehensive personal relationship managers. These employees must understand a wide array of complex digital products. Customers facing an overwhelming number of financial choices desperately need expert guidance. A trusted financial advisor helps clients confidently navigate this confusing digital landscape. The human element remains crucial for building long-term financial trust.

Despite the current wave of Cincinnati bank closures, some institutions are selectively expanding. Banks continually open new smart branches in highly targeted suburban markets. These modern locations feature state-of-the-art technology alongside expert financial planners. The ultimate goal provides a premium, customized experience for high-net-worth individuals. Therefore, the physical bank branch survives by reinventing its core purpose. Cincinnati customers must adapt quickly to this new era of modern financial services.

FAQs

Why are banks closing so many physical branches in Cincinnati?

Banks are consolidating branches to reduce the high operational costs associated with maintaining physical locations. An in-branch transaction costs a bank approximately $4.00 to process, whereas a digital transaction costs only about four cents.

How do these branch closures impact local communities?

The shutdowns are creating banking deserts that disproportionately affect rural areas and lower-income urban districts. This rapid transition creates significant challenges for cash-heavy small businesses and older adults who rely on in-person assistance.

What local alternatives are available for residents?

Residents can transition their accounts to community banks and non-profit credit unions, which continue to maintain a strong physical presence in neighborhoods. Alternatively, consumers can use digital-only banks, though depositing physical cash often requires visiting a third-party retailer that may charge a fee.

What is the future role of physical bank branches?

Surviving branches will transition away from processing routine daily transactions and operate instead as specialized advisory centers. Staff will focus primarily on complex financial problem-solving, including mortgage origination, retirement planning, and wealth management.